/Group%20142.png?width=675&height=470&name=Group%20142.png)

/img.png?width=600&height=401&name=img.png)

/Mask%20group.png?width=600&name=Mask%20group.png)

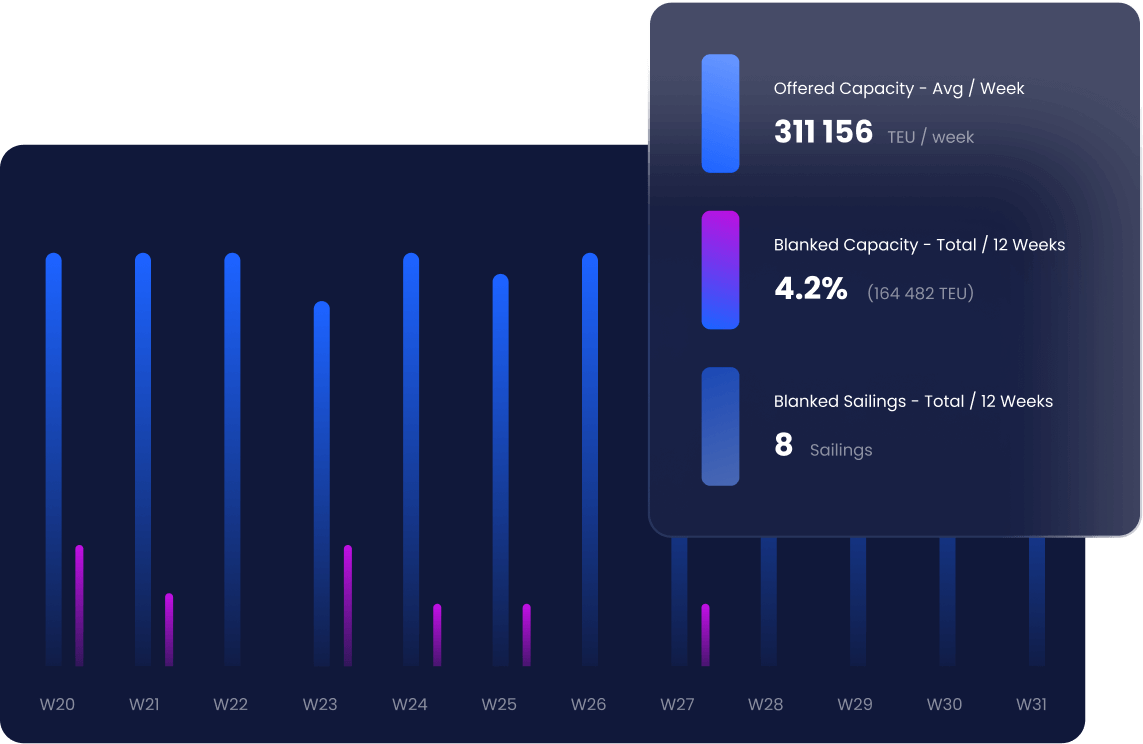

Shippers

Shippers using Xeneta see an average reduction in annual freight spend of 6.5%. Using the Xeneta platform to monitor the market, report and align internally, identify opportunities and risks, and inform your budgeting and tender decisions is key to a leaner, smarter, agile supply chain.

Xeneta for Shippers

/graphic.png?width=1145&height=754&name=graphic.png)

.png?width=387&name=Blog%20Banners%202022%20(4).png)