The Transatlantic air cargo market has been overlooked by many during 2024 due to the dramatic developments on ex-Asia corridors, but skyrocketing rates during peak season puts it back in the spotlight with shippers facing a dilemma over new contract negotiations.

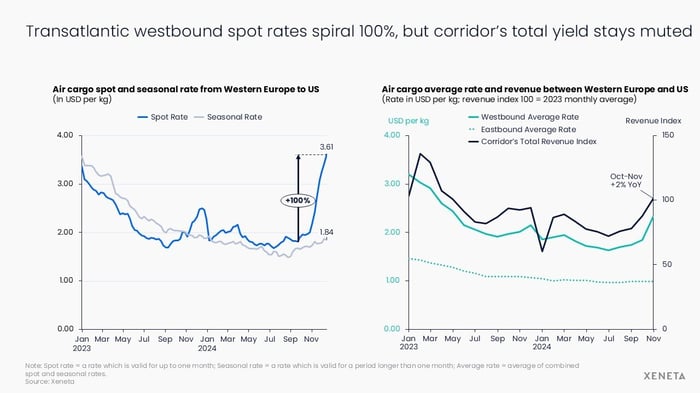

In the week ending 15 December, the average air cargo spot rate from Western Europe to the US (valid for up to one month) surged to USD 3.61 per kg. This marks a 100% increase compared to the start of this year’s peak in late September and represents the highest rate recorded in over two and a half years.

Around 50% of the volume on this corridor is sold on the spot market.

Developments on the spot market are in stark contrast to the westbound seasonal rate (valid for over one month), which only showed a modest increase of 10% since the start of peak season and dropped 4% from a year ago.

Why did rates sky-rocket?

Air cargo demand has been muted on this corridor, so the spot rate spike can be attributed more to factors relating to supply.

These factors include airlines’ winter schedules seeing reduced passenger belly capacity and slight capacity dip during Thanksgiving holidays in the US.

There is also the impact of airlines moving capacity off traditional established air cargo trades such as the Transatlantic to meet the increasing demand on ex-Asia corridors where e-commerce is booming.

The impact of ex-Asia e-commerce on these trades was one of the key themes in Xeneta’s Air Outlook 2025 report, published last week. Download your copy here.

Consequently, air cargo capacity from Western Europe to the US fell 5% in mid-December compared to the same period in 2023 and down 15% from pre-winter schedule levels two months ago.

Additionally, spot rate increases on the Transatlantic westbound market may stem from a trade imbalance on the backhaul from the US to Western Europe, where cargo average rates dropped 4% year-on-year.

In the first two months of Q4, the overall cargo revenue growth for both westbound and eastbound trades combined was just 2% year-on-year. This means it becomes even more important for airlines to increase revenue on the fronthaul.

Pressure on capacity

The dynamic load factor from Western Europe to the US stood at 80% in the first half of December, way above the weight load factor of 55%, a traditional load factor measurement.

The 80% dynamic load factor marks a year-on-year increase of 3 percentage points, and a much larger 10 percentage points compared to two months ago.

Note: Dynamic load factor is Xeneta’s measurement of capacity utilization based on volume and weight of cargo flown alongside available capacity.

Xeneta predicted the dynamic load factor would hit the 80% on this corridor in a shift that signals a shift from a buyer’s market to a seller’s market, with increasing negotiating power for freight sellers. Historically, such fundamental changes in negotiation dynamics often result in non-linear impacts on freight rates. For instance, during previous periods when the transatlantic market reached 80%—notably in 2020-2022 and 2018—freight rates experienced exponential growth.

As always, it is important to use data to monitor market development at an airport as well regional level because when focusing on Transatlantic corridors into Chicago (ORD) the load factor stood at a higher 85%.

What next and where does this leave shippers?

As the year draws to a close, Western Europe to US spot rates are expected to decline in the coming weeks, following air freight's cyclical patterns.

However, market sentiment has shifted considerably from a year ago and shippers must consider more than seasonal and regional patterns, especially given the gravitational pull e-commerce out of China seems to have on available air cargo capacity.

Shippers who secured contracts before the recent rate surge may feel temporarily insulated from the escalating market, but they will likely face pressure during the upcoming tender season.

Freight forwarders – currently under intense pressure to maintain operations for volumes without block space agreements – will likely pass at least some of their increased costs on to customers.

On top of this, the implementation of the ReFuelEU sustainable aviation fuel (SAF) mandate on 1 January 2025 (requiring fuel suppliers at EU airports to include a minimum of 2% SAF) will increase costs for airlines.

The potential second round of US East and Gulf Coast port strikes from 15 January will surely drive up air freight rates further in this corridor (if it happens).

How do shippers approach this uncertainty?

Firstly, it is more important than ever that shippers take a holistic view of global air freight market, understanding that risks can originate far outside the bounds of the corridors they use to transport goods.

To navigate such market dynamics, it is recommended for shippers to keep a close eye on airline sell rates (available in the Xeneta platform) to get an early indication on how freight forwarder sell rates for shippers are likely to develop.

This will be vital information when forming a strategy for new contract negotiations.

Shippers may also be wise to consider extending existing contracts further into Q1 next year when the rates ease - negotiating when the market is hot can strengthen the hand of the vendor.

Additionally, staying flexible and considering importing goods into alternative airports is recommended – the example of dynamic load factor into ORD demonstrates the variances within corridors.

Finally, with the potential volatility anticipated in 2025, proactive planning in specific markets will be crucial to mitigate buying capacity in the short-term market. Shippers exceeding their allocated volumes may risk being pushed onto the escalated spot market.